This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Credit bureaus , which were very localized at the time, began expanding to a more national footprint. Expanding these bureaus nationally enabled standardization in credit assessments. Banks also began adopting statistical methods and metrics to assess creditrisk.

But making heads or tails of your business creditreport can be tricky. What is a Business CreditReport? There are three main business creditreportingagencies: Dun & Bradstreet (D&B), Experian , and Equifax. This is really no different than the concept of a personal creditreport.

Your business credit score affects your ability to get loans, enter into leases, and make purchases—and since other businesses, banks, and lenders can check it at any time without your permission, you want to make sure that it’s completely accurate. But making heads or tails of your business creditreport can be tricky.

Monitoring risk is crucial to mitigating it. Trust Command Credit Business CreditReports. When you buy business creditreports at Command Credit, you can choose reports from multiple business creditreportingagencies, including Experian, Equifax, Dun & Bradstreet, TransUnion, and CreditReports World.

Since entrepreneurs and new business owners are typically very invested in launching their business, lenders instead look at individual credit scores and creditreports to gauge creditrisk. The stronger your personal credit, the more likely you’ll receive an approval for your first business credit.

The Major Business CreditReportingAgencies The job of a business creditreportingagency (also called a business credit bureau) is to gather information about your company. A credit bureau gathers details from your previous creditors and other sources and puts that data into a business credit file.

In the business credit world, there are five main creditreportingagencies. These credit bureaus gather information about your company and resell it to others that want to predict the risk of loaning money to your company. It’s wise to understand who the business credit bureaus are and how they operate.

The first option involves directly contacting the lender regarding the potential error on your payment history, such as a credit card company or student loan issuer. The next option involves filing a dispute with the creditreportingagency regarding the possible erroneous entry.

There are dozens of places where you can obtain your creditreport. The three big credit bureaus, however, are Equifax®, Experian®, and TransUnion®. Often referred to as creditreportingagencies, these companies work independently. CreditReports vs. Credit Scores.

The business creditreportingagency also maintains commercial creditreports on over 300 million businesses around the globe. The process and cost of checking your consumer and business credit scores, however, can differ in several ways. Higher scores signal the opposite.

The goal of the organization is to serve the business lending industry by providing accurate and reliable data to help lenders predict small business creditrisk. Business creditreports that contain data from the SBFE might make or break your future business credit applications. How Does the SBFE Work?

VantageScore vs FICO Most people use the terms credit score and FICO Score the same way, but there’s more than one type of credit score. Both are valid and used by multiple types of lenders to determine your likelihood of repaying debts and creditrisk. A variety of versions are used from each creditreportingagency.

Equifax’s three primary business credit scores are their CreditRisk Score, Payment Index Score, and Business Failure Score. A good CreditRisk Score or Payment Index Score generally indicates that your business is likely to make its payments on time. Next, let’s touch briefly on the Payment Index Score.

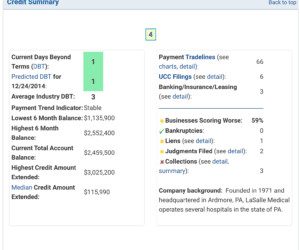

The key metric displayed on a business creditreport is a business credit score. Each creditreportingagency will use slightly different scoring criteria and algorithms, but this score will let you know at a glance the credit-worthiness of a company. The credit limit is also displayed here.

Yet lenders that use PayNet Scores will typically consider a PayNet MasterScore of 700 or higher to indicate a low level of creditrisk. PayNet® is a business creditreportingagency that maintains a database of more than 25 million small business contracts — small business loan accounts, business leases, and business lines of credit.

FICO’s website offers a helpful chart showing which industries, lenders, and credit-reportingagencies use each type of FICO Score. They also point out that the basics of excellent credit remain the same: make payments on time, keep your balances low, and only open new credit accounts when needed.

But a business’s creditreport can be pulled at anytime without that business needing to give permission. There are numerous creditreportingagencies, which charge varying amounts for each report, and collect different information. Dun & Bradstreet.

They are made up of various credit ratings, scores, and statistics, ranging from predictive (for the future) to performance-based (historical), that can be used to demonstrate a business’s dependability and financial stability. In case you purchase any company creditreport it should contain the following information.

The trade-off for having your debt eliminated is a long-lasting derogatory mark on your creditreport identifying you as a huge creditrisk. Your creditreport sees the effects of a bankruptcy filing for ten years for a chapter 7 bankruptcy. Will My Credit Score Increase After Bankruptcy Falls Off?

For any organization looking to minimize creditrisk and increase profitability, it is essential to comprehend how trade references operate and how to use them successfully. It is an essential tool for organizations to assess creditrisk and decide whether to issue credit. What is a Trade Reference Meaning?

business loan, business credit line, etc.), A business creditreportingagency can also use your EIN to open a business credit file for your company. Request a DUNS Number Before your business can qualify for certain types of funding, you will need to establish business credit scores.

Over the past two decades, the financial services industry has been gravitating towards a more comprehensive approach to creditrisk assessment. Credit scoring models alone don’t tell the whole story, so companies are looking to alternative credit data to fill in the gaps. Here are a few examples.

Unlike a consumer credit score, which uses a fairly standard ranking system, business creditreporting bureaus use different data sets. So, what is a good business credit score ? It depends on which credit bureau you use. What Is a Good Business Credit Score? Equifax Business CreditRisk Score.

If you own or operate a business and if you have borrowed money, bought supplies on credit, or extended credit to a customer, there is almost certainly information about your business stored in the databases of the business creditreporting bureaus. The most important thing you need to do is pay your bills on time.

Business creditreports help you: See signs of deteriorating financial health Manage business creditrisk Forecast and manage your cash flow Make better decisions about extending credit and on what terms. Get Experian Business CreditReports.

We get that, for many small business owners, raising your credit score can feel like just another thing on top of a huge stack of to-do’s. Plus, knowing that there are three main business creditreportingagencies ( Experian , Equifax , and Dun & Bradstreet ) can feel a bit overwhelming.

Unfortunately, derogatory marks cause your credit scores to drop and alert future creditors that you present a higher creditrisk. However, they don’t stay on your reports indefinitely and tend to have a diminishing impact as time passes. Here’s a look at their current reporting timeframes.

Computed through a blend of factors like payment history, credit utilization, public records, and more, business credit scores are the backbone of informed lending decisions. Notably, there are several creditreportingagencies, each with its scoring model.

However, more options are typically available to borrowers with thin credit profiles than to borrowers with a bad credit score because of a historical poor repayment history. There are many different types of credit scores, as providers create them to serve different purposes. What Is a FICO Score?

Other Business Credit Scores Depending on the lender, they may also use other proprietary business credit scores generated by the major business creditreportingagencies. There’s also the Equifax Small Business CreditRisk Score, which ranges from 101 to 992.

However, more options are typically available to borrowers with thin credit profiles than to borrowers with a bad credit score because of a historical poor repayment history. There are many different types of credit scores, as providers create them to serve different purposes. What Is a FICO Score?

Here is an explanation of the different options that are available through Command Credit, the lowest-priced provider of business creditreports from all of the major business creditreportingagencies. Buy Business CreditReports: The Self-Serve Option.

The first negative information that appears on your creditreport is entries regarding late payments or missed payments that are reported to the creditreportingagency. This is one reason why “maxing out” a credit card is generally discouraged.

Lenders perceive consumers with high credit utilization ratios as potential creditrisks, as they may be “overextended.” According to Experian, credit utilization ratios of less than 30% are typically considered as good.

Experian provides business credit scores designed to predict the likelihood that a business will have serious credit delinquencies in the next year. Similar to how personal credit scores are used, third parties like lenders look to business credit scores to figure out how much creditrisk a business presents.

You can use the funds within the credit limit for your own purposes. This makes primary user tradelines the most preferred type with lenders and credit bureaus because it’s a more accurate representation of your true creditrisk.

While you can (and many lenders who require personal guarantees will check your FICO), relying purely on personal credit is not going to offer you all the same advantages. A business credit score is based on the financial track record of your business, and is tied to your employer identification number (EIN).

This is essential for them to consider you a good creditrisk when offering you a business loan for rental property. In order to verify that you are an acceptable creditrisk for them, lenders want to see both personal and business information that demonstrates your business knowledge and financial stability.

Outstanding balances on credit accounts Credit utilization (the percentage of your credit limit you’ve used) Public records Company demographics Tradeline trends over time When looking at the major creditreportingagencies for consumers, the same is true. Is cash flow data the future of credit?

It’s also important to understand that you don’t have just one credit score—different lenders and creditreportingagencies use multiple credit scores. These bureaus, in turn, gather information from lenders like credit card companies, student loan lenders, and banks.

Like most credit scoring models, a higher number means youre more likely to repay your debts as promised. A score in the mid-to-high 200s typically indicates that youre a good creditrisk. On the other hand, a low SBSS score could cause you problems in business credit decisions. Who is the FICO SBSS Score Used By?

New lenders or suppliers might also review a trade reference letter when you fill out a credit application. Looking over your past payment history on other accounts can help these businesses determine whether your company is a good creditrisk. They can help your company establish positive business credit.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content