This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Having a healthy creditscore is more than a financial achievementits your gateway to better credit card deals, lower interest rates, convenient loan terms, and even housing options. In this article, we show you how to clean up your creditscore and improve your score quickly after the cleanup.

Credit builder cards assist in growing or rebuilding your credit and can help you stay on track to improve your creditscore. Understanding how these cards work and knowing what to look out for will be useful in choosing one that helps you establish credit, qualify for loans, and unlock exclusive rewards.

Your FICO score isnt a random number lenders like to ask aboutits a gateway to a more secure financial future. Your creditscore is a reflection of your financial activities and behaviors, a useful tool for opening doors to financial opportunities or a roadblock to achieving your financial goals.

Most of us are familiar with the concept of checking our creditscore—and, luckily, it’s a fairly simple process these days (for instance, you can do it right here). It’s true—even though you might think that a business creditscore is just, well, private business , it’s actually publicly accessible.

Looking to learn the ins and outs of Experian business creditscores ? as a consumer credit reporting company, but it also collects information on millions of businesses and provides business credit reporting services. You can download the Tillful iOS app to check if your company has a credit profile with Experian.

Often referred to as credit reporting agencies, these companies work independently. Credit Reports vs. CreditScores. Your creditscores are also influenced by your credit reports. The reason for this is that creditscores are calculated using information from your credit report.

What’s more, on Main Street, most bankers are just as interested in your personal credit rating as your business rating—sometimes even more. Minimum CreditScore By Loan Type Lenders look at both business and personal creditscores when reviewing small business financing applications.

Have you heard about the FICO Small Business Scoring Service (SBSS)? Like most business creditscores, the SBSS helps lenders and service providers understand the level of credit risk that businesses present. Here’s a closer look at FICO SBSS scores, why they matter, and how you can improve yours.

As a result, this prevents harming your creditscore or even bankruptcy. Understand creditscores. Lenders use a creditscore between 300 and 850 to figure out how likely you are to repay debts,” explains Due Founder and CEO John Rampton. Your creditscore will be pulled instead,” adds John.

Life’s uncertainties—job loss, emergencies, foreclosures, bankruptcies—can severely damage credit. With a commitment to bouncing back, discipline, careful planning, concrete goals, and strategic choices, it is possible to recover from financial troubles and rebuild your credit status.

Back then, you built your credit in anticipation of applying for credit cards, buying a home, leasing a car, taking out loans, etc. Without a good creditscore and excellent credit history , you would not be able to achieve all of that. Hopefully, you kept at it to build and maintain a great creditscore.

And that all boils down to the idea that the best candidates for local business loans present the lowest risk to the lender. If you want to be the best possible candidate for a local business loan, credit is king. You have a business creditscore, right? But, as with all things credit-score related, the higher the better.

Over the past two decades, the financial services industry has been gravitating towards a more comprehensive approach to credit risk assessment. Creditscoring models alone don’t tell the whole story, so companies are looking to alternative credit data to fill in the gaps. Here are a few examples.

A credit repair company will dispute any negative information that was incorrectly reported on your behalf with the intent of having the adverse entry deleted or modified in a way that reflects favorably on the consumer. Experian states how some unscrupulous companies in the past tarnished the credit repair industry’s reputation.

A derogatory mark on a credit report refers to a negative item such as a late payment, a loan default, a repossession, or a foreclosure. Unfortunately, derogatory marks cause your creditscores to drop and alert future creditors that you present a higher credit risk. Bankruptcy filings : Five years.

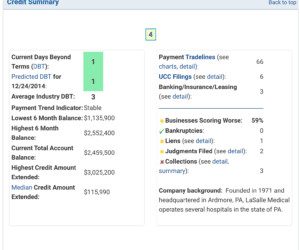

Credit is a fundamental business tool that allows companies of all sizes to keep operations running smoothly, invest in expansion, and work with their partners and vendors. Traditional business creditscores work off key indicators that they’ve determined to accurately reflect a company’s financial strength and creditworthiness.

Despite the fact that a business credit report can provide important information about a company’s financial health, many businesses aren’t fully aware of what it is. This business creditscore shows that you have good money management skills and the ability to pay back any loans you obtain on time.

Your first credit card is an essential step on the path to financial empowerment. It can help you develop critical financial skills, establish your creditscore, and give you financial flexibility. Let’s look at some of the things you should look for when selecting your starter credit card. .

In addition to increasing account balances, late fees can negatively affect consumers’ creditscores as well. Credit cards are one of the best ways to earn rewards and take advantage of zero-interest rate promotions. Focus on one credit card for creditscoring purposes, but keep them open for other purposes.

If you default on your “loan” with a pawnbroker, your creditscore won’t report it—but technically, this is a form of alternative lending. Alternative lenders, on the other hand, accept entrepreneurs with shorter times in business, lower creditscores, less proven revenues and cash flow…. More Frequent Repayments.

In a world that constantly bombards people with images of wealth and success, it’s no wonder to feel the pressure of presenting a facade of wealth. Living beyond one’s means can lead to maxed-out credit cards, personal loans, and even bankruptcy. The long-term consequences of debt can be devastating.

million views and counting, FinTok’s content creators, also known as “finfluencers,” tout this rule as a credit payment system that improves your creditscore. Before we find out, you must learn a basic principle about credit cards and lines of credit: the credit utilization ratio.

While your revenue and creditscores haven’t changed, your application gets rejected. This can happen as the result of a credit crunch — also called a credit crisis or credit squeeze. What is the difference between a recession and a credit crunch ? What should you do if you can’t qualify for business credit?

But working with online alternative lenders presents a great opportunity for business owners to obtain financing quickly, affordably, and under realistic qualification standards—something that for more than a decade now has been all but impossible through a traditional bank. FICO CreditScore: Fundbox doesn’t check your creditscore.

Before you apply for a loan through Lendistry , however, do know that for traditional business loans, Lendistry won’t accept businesses that have declared bankruptcy within the last three years or business owners who have defaulted on government debt. For larger lines, business owners will need at least a 680 FICO score, $1.5

Nicolosi says that alternative lenders mainly evaluate their short-term applicants based on creditscore, sales, profitability, and time in business. 600+ personal creditscore. They’re also looking for strong personal credit and an applicant who hasn’t declared personal or commercial bankruptcy in the past five years.

To be considered for a Kiva loan, you don’t need the minimum personal creditscore , time in business, and profitability that most other lenders need to evaluate before extending you a loan. You’re not currently in foreclosure, bankruptcy , or under any liens. You won’t need to provide collateral , either.

Because consumer debt is routinely reported to major credit bureaus like Equifax, Experian, and TransUnion, it may have an effect on a customer’s creditscore. With this strategy, you must examine your invoice creation process and ensure that each of the elements listed below is present: A billing date.

These funds could be used to pay off a credit card debt or pad your savings. When a few dollars separate you from foreclosure or bankruptcy, every dollar counts. Your creditscore is 579 or lower. In this case, additional credit is difficult to get at a reasonable interest rate as this is below the average.

You know your creditscore plays a big part in this but what about your credit history, debt to income ratio, additional assets, and employment status? CreditScore The creditscore requirements depend on which type of loan you choose as well as which lender you decide to work with. 50% to 3.6%

These funds could be used to pay off a credit card debt or pad your savings. When a few dollars separate you from foreclosure or bankruptcy, every dollar counts. Your creditscore is 579 or lower. In this case, additional credit is difficult to get at a reasonable interest rate as this is below the average.

You know your creditscore plays a big part in this but what about your credit history, debt to income ratio, additional assets, and employment status? CreditScore The creditscore requirements depend on which type of loan you choose as well as which lender you decide to work with. 50% to 3.6%

Expect your credit to have a greater influence on whether you will qualify than your current income will. Some landlords only check credit reports for red flags like recent evictions. Others check creditscores too and have minimum creditscore requirements. What is a Bad CreditScore for Renting?

Also, certain negative items on your credit report, such as a recent bankruptcy or foreclosure, can pose a significant challenge. If you’re denied because of credit reasons, consider working to improve your business creditscores before you apply for any type of financing.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content