This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Another reason why Americans have so much medical debt is that many Americans have high-deductible health insurance plans. These plans have a low monthly premium, but they have a high deductible, which is the amount of money that the insured person must pay out-of-pocket before their insurance starts to pay.

If youre about to apply for a mortgage loan, you are most likely concerned about how the loan will affect your creditscore. This is because your creditscore significantly influences your financial prospects and your chances of qualifying for loans, lower interest rates, cash back rewards, and travel points.

To make matters worse, invoice errors also tend to generate payment deductions (partial payments). Correcting invoices and reconciling payment deductions are essentially rework: work that is not necessary if you got it right the first time. To make matters worse, most payment posting errors will involve deductions.

Repayments are typically made through daily or weekly deductions from the business’s bank account or directly from credit card sales. Qualification Criteria MCA : Often requires a strong credit card sales or bank deposit history and minimum creditscore/ time in businesses.

This is done by getting updated credit reports, updating credit references, sharing information with a credit industry group, and monitoring various information sources both internal and external. When you become aware of suits, liens, judgments, slowing payments or deteriorating creditscores it is time to take action.

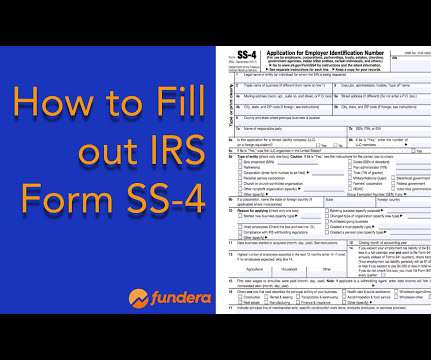

If you file for bankruptcy. Plus, for certain types of tax deductions, such as home office deductions for business, your chances of an IRS audit decrease if you have an EIN. “If Personal office deductions have a tendency to bring on IRS audits. Corporations and any entity taxed as a corporation. Multi-member LLCs.

If you file for bankruptcy. Plus, for certain types of tax deductions, such as home office deductions for business, your chances of an IRS audit decrease if you have an EIN. “If Personal office deductions have a tendency to bring on IRS audits. Corporations and any entity taxed as a corporation. Multi-member LLCs.

Get a handle on your personal and business creditscores. We’ll break down need-to-know accounting terms, how to handle your creditscores, how to apply for a business loan, and more—so that you’ll have all the information you need to manage your small business finances. Gross Revenue. Net Profit.

Unfortunately, regardless of the reason, they will affect your creditscore. Still, you may be wondering—how long do late payments stay on your credit report? Still, you may be wondering—how long do late payments stay on your credit report? How Does a Late Payment Affect Your Credit?

Late payments remain on your credit bureau report and influence your creditscore for seven years. Fortunately, there are ways to improve your overall credit profile to offset the adverse results that late payments have on your creditscore. and 35% of your FICO score.

“We do not make a judgement on your application based solely on your creditscore,” says Walpert. Payment Frequency: Loan payments get deducted from your business checking account on the 1st and 16th of each month. Approval Time: Typically you’ll have your loan decision within 48 hours of receiving all documentation.

Your credit history sums up all the information in your credit report. This information includes balances due, credit accounts, and payment history details. Your credit report also contains information on overdue debt, foreclosures, bankruptcies, judgments, and liens. FICO scores range from 300 to 850.

In addition to increasing account balances, late fees can negatively affect consumers’ creditscores as well. It’s easier to review your policies with one insurer and see at a glance if your limits and deductibles are appropriate for your needs,” Penny Gusner, consumer analyst at Insurance.com, told Kiplinger.

Get ready to learn about need-to-know accounting terms, managing your creditscores, applying for a business loan , and more so you can feel prepared for managing finances for a small business. Part 3: Get a Handle on Your CreditScores. How to Manage (and Boost) Your Personal CreditScore. Gross Revenue.

Get ready to learn about need-to-know accounting terms, managing your creditscores, applying for a business loan , and more so you can feel prepared for managing finances for a small business. Part 3: Get a Handle on Your CreditScores. How to Manage (and Boost) Your Personal CreditScore. Gross Revenue.

If they’ve ceased operations and left debts unpaid, you might struggle to recover your money, especially if there are no remaining assets or if the business owner declares bankruptcy. This means keeping an eye on key indicators like creditscores, payment histories, and any signs of financial distress. What can you do?

You can opt to automate some of the steps with tools, such as: Business creditscore/ financial health tracking : Tillful’s free business creditscore service lets you log in at any time to get a snapshot of your business’s financial health. It also gives you free access to your Experian business creditscore.

Living beyond one’s means can lead to maxed-out credit cards, personal loans, and even bankruptcy. In 2020, there were over 544,000 bankruptcy filings in the United States, many of which stemmed from unmanageable debt. Include your net income (the amount you take home after taxes and deductions).

It’s hard to quantify your character, but Wells Fargo does so with your personal creditscore. And if you don’t have a personal credit history, Wells Fargo might consider any personal references, business experience, or work history as a substitute.). Bankruptcy. They’re hard to qualify for.

And if your lack of working capital gets really bad, then it could lead to bankruptcy. A merchant cash advance is a quick, easy way to get a business cash advance with no need for collateral—even if you don’t have a great creditscore. It’s important to catch low working capital before it gets out of hand.

Credit Fee $50 $2.69 $2.50 $2.50 $100 $2.69 $2.50 $2.50 $250 $4.63 $4.68 $4.95 $1,000 $18.50 $18.70 $19.80 $2,500 $46.25 $46.75 $49.50 $10,000 $185.00 $187.00 $198.00 As a result, they are tax deductible for business owners. Scoring algorithms look at the total amount of credit you have available compared to the amount you’ve used.

Because consumer debt is routinely reported to major credit bureaus like Equifax, Experian, and TransUnion, it may have an effect on a customer’s creditscore. This thorough paperwork will also be useful if you choose to deduct bad debts from your taxes.

These funds could be used to pay off a credit card debt or pad your savings. When a few dollars separate you from foreclosure or bankruptcy, every dollar counts. Your creditscore is 579 or lower. In this case, additional credit is difficult to get at a reasonable interest rate as this is below the average.

Improve your creditscore. Creditscores are a snapshot of your finances. Creditors look at your score as a sign of trustworthiness. If you’ve got a high creditscore, you’re more likely to be able to handle your finances and repay debt; if you’ve got a low score, you’re more risky.

These funds could be used to pay off a credit card debt or pad your savings. When a few dollars separate you from foreclosure or bankruptcy, every dollar counts. Your creditscore is 579 or lower. In this case, additional credit is difficult to get at a reasonable interest rate as this is below the average.

All federal student loans entail a one-time origination fee deducted from your loan funds. However, to qualify for this private refinance, they need a robust creditscore, sufficient income to make the necessary payments and a solid track record of on-time loan payments.

Improve Credit Onboarding Automation and Controls: Provide a customizable credit application portal for new accounts that requires the documentation and an appropriate customer credit application to be completed fully and accurately prior to submission to the credit department. Consider a third-party service.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content