This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Monitoring and evaluating the creditrisk posed by public companies and other large firms differs significantly in comparison to small and mid-sized businesses. Because most of your biggest customers will be larger firms instead of smaller, it is typically the larger firms that will require higher credit limits.

Credit management takes center stage when: New customers apply for credit terms. There needs to be a determination of the risk of the new account going delinquent or defaulting in accordance with your firm’s tolerance for creditrisk. it just might help them collect faster and pay you sooner.

After, the Great Recession of 2008, commercial bankruptcies peaked in 2009 and did not drop below pre-recession levels until 2012. Department of Justice projects a substantial increase in bankruptcy filings. Trustee Program has estimated that bankruptcy filings will double over the next three years.

This company was fortunate to avoid significant bad debt loss until Ames Department Stores, Kmart, and Fleming Foods (a distributor) all filed bankruptcy within the same year. Learn More About Credit Reports Please share this newsletter with your smallbusiness customers. Bad debt losses were understandably huge.

While multiple factors can contribute to an organization's financial downfall, insufficient cash flow is typically the primary trigger for bankruptcy proceedings. Learn More About Credit Reports Please share this newsletter with your smallbusiness customers. it just might help them collect faster and pay you sooner.

This company’s evaluation of the risk/reward tradeoff was flawed because it underestimated the creditrisk of “large” enterprises. If you doubt that, look at the number of leading companies who filed bankruptcy in recent years. Creditworthiness should never be taken for granted. Share Read more

Abrigo's most popular whitepapers and checklists on lending and creditrisk Abrigo experts' insights on CFPB 1071, loan policies, and risk ratings were popular with banking professionals. You might also like this webinar, "Unraveling risk rating: Making sense of your best early warning tool." Here are the top resources.

Running a business involves a constant learning curve. And that applies whether you’re a rookie entrepreneur just starting out with a great idea for a new business or a more established smallbusiness owner with a quickly growing business that needs to expand. Accounting Terms to Know. Accounts Receivable.

Furthermore, new businesses and smallbusinesses tend to have high failure rates, and there is good reason to believe a wave of defaults is coming. Among other things, commercial bankruptcies have been steadily climbing over the past year. Please feel free to share this newsletter with your smallbusiness customers.

Commercial bankruptcies have been surging since mid-2022. Chapter 11 filings, used by businesses hoping to reorganize, have increased by 34 percent in the first six months of 2024 compared to last year. Department of Justice expects a sharp increase in bankruptcies with the U.S. And the future is bleak — the U.S.

Photo by Melinda Gimpel on Unsplash ) The American Bankruptcy Institute recently reported that, “The 6,067 total commercial chapter 11 bankruptcies filed during the first nine months of 2024 represented a 36 percent increase over the 4,561 filed during the same period in 2023.” Trustee Program. Share Read more

The point is: receivables are an investment that needs to be managed with regard to the inherent risks associated with AR. Failure to deal with those risks is not investing, or managing, but rather simply gambling. Please feel free to share this newsletter with your smallbusiness customers.

Here are some factors AR managers should anticipate: Interest rates may ease somewhat, but the days of easy money are over for the foreseeable future — working capital management is extremely important now Commercial bankruptcy filings are expected to continue rising (the U.S. it just might help them collect faster and pay you sooner.

Adding to the credit grantor’s challenge, that line is constantly changing. Please share this newsletter with your smallbusiness customers. Share Determining Creditworthiness For these reasons, creditworthiness is a fundamental consideration when granting credit to a business customer.

Growth is down, interest rates continue rising, smallbusinesses are facing a credit crunch, commercial bankruptcies are skyrocketing and experts see an emerging threat: Washington Post: U.S. A critical part of this exercise involves identifying active and new customers posing high, or even just marginal, creditrisks.

Older debts are often more difficult to recover because the debtor’s financial situation may worsen over time, or the business may close, become insolvent, or declare bankruptcy. In cases of bankruptcy or liquidation, the likelihood of repayment drops dramatically, as creditors may only receive partial payments or nothing at all.

For instance, bankruptcy within the next two years is more easily defined than the more nebulous state of financial distress. Despite these shortcomings, commercial credit scores can be valuable tools for a company offering trade credit to other businesses. it just might help them pay you sooner.

While bankruptcy filings have not increased substantially in the past year, they have begun to tick up and it is widely anticipated that filing will continue to increase as pandemic relief is finally spent, revenues decrease due to a faltering economy, and costs increase due to inflation and rising interest rates.

Running a business involves a constant learning curve. And that applies whether you’re a rookie entrepreneur just starting out with a great idea for a new business or a more established smallbusiness owner with a quickly growing business that needs to expand. Business Finance Terms and Definitions to Know.

Without open terms, business cash flows would be restricted, with the lost liquidity acting as a break on the velocity of commerce. Photo by Jamie Street on Unsplash There are two types of creditrisk that arise from selling on open credit terms: Customers paying beyond terms (past due) reduce your cash flow.

Under-performing AR has the potential to create a cash flow crisis that can shut down your business in very short order. Cash Flow is the number one cause of smallbusinessbankruptcies. Please feel free to share this newsletter with your smallbusiness customers. it just might help them pay you sooner!

Commercial bankruptcies have been trending upward for most of this year, so it is likely some of your customers are in a downward spiral, if it has not yet shown up in their payment pattern. Recognizing that a customer is in distress putting your receivables at risk is the first step in ameliorating the situation.

Subscribe now Learn to Recognize These Red Flags There are two types of creditrisk affiliated with selling on open credit terms. If you have more than a few customers or you have been in business several years, chances are you have dealt with customers who pay late, have defaulted or are at risk of default.

Extending credit to customers is not only common, but necessary for most companies. However, every time you extend credit to a customer, you are taking a risk. A big part of your job, whether you are a smallbusiness owner or an executive at a large enterprise, is managing risk — especially preventable ones.

Have you heard about the FICO SmallBusiness Scoring Service (SBSS)? Like most businesscredit scores, the SBSS helps lenders and service providers understand the level of creditrisk that businesses present. smallbusinesscredit applicants. What is an SBSS score?

In addition, extended terms increase your exposure to customer bankruptcies and the resulting non-payment. If a customer has 60 day payment terms, and pays 30 days late, you will have three months of sales dollars at risk versus one if the customer had 30 day payment terms. it just might help them collect faster and pay you sooner.

Why You Should Know How to Check the BusinessCredit Scores of Other Companies. According to credit bureau Experian, as of 2015 upwards of $8 billion is lost or stolen from smallbusinesses yearly due to fraud. As a smallbusiness, you depend on your customer’s ability to pay their bills.

While there’s some debate in American politics over whether or not “corporations are people,” it is true that businesses have credit scores and can receive credit reports the same way individuals do. A short list of factors affecting your score also includes: Credit utilization ratio. Length of credit history.

Often, small orders are better handled on cash in advance terms or via a credit card transaction rather than the granting of open credit terms. Please feel free to share this newsletter with your smallbusiness customers. Smallbusinesses are less risky customers than large businesses.

If you’re a smallbusiness owner, you have two credit scores. There’s your personal credit score, and then there is your businesscredit score. A businesscredit score is a reflection of the creditworthiness of your business. Your Payment Index score is your typical credit score.

Plus, if you ever experience problems with one of your businesscredit reports (i.e. identity theft, credit errors, etc.), knowing which businesscredit bureau to contact might help you resolve the issue faster. Below is an overview of the five primary businesscredit bureaus.

While there’s some debate in American politics over whether or not “corporations are people,” it is true that businesses have credit scores and can receive credit reports the same way individuals do. A short list of factors affecting your score also includes: Credit utilization ratio. Length of credit history.

Variable requirements might include a minimum credit score or monthly income, some deposit or asset for securing the loan (collateral), a specified debt-to-income ratio, and others. Business Loans Smallbusiness owners might qualify for some type of business loan.

Report users can purchase businesscredit scores from Equifax too, such as: Business Delinquency Score Business Delinquency Financial Score BusinessCreditRisk Score Early Default Score And More Different business scoring models have different numerical ranges.

According to the US SmallBusiness Administration, your company will require a credit score of around 75 to qualify for a smallbusiness loan. Credit scores can also affect a company’s ability to sign a lease or purchase products on credit from suppliers. “

Why Does a Good BusinessCredit Score Matter? Without a good credit score, smallbusinesses are more likely to be denied financing, provided lesser amounts than requested, and/or face more burdensome lending terms, such as higher interest rates and shorter payback periods. Paid: $99.95

Or why SBA loans, the crème de la crème of smallbusiness loans, require so much documentation? You’re probably aware that good businesscredit comes with perks, but it might be less clear as to why. Well, it all comes down to creditrisk. What is CreditRisk? Borrower Reputation.

Like your personal credit, it should be something you prioritize, monitor regularly , and leverage to help ensure the best possible financial performance and opportunities for your smallbusiness. That will tell you which bureaus you have documented credit history with. Main Factors in the Equifax BusinessCredit Report.

Even before you began your search for smallbusiness loans , you’ve more than likely heard of a credit score. You’ve also more than likely heard of a good credit score, too. Here’s the gist of it: Your credit score is a numerical indication of how responsibly you’ve handled your financial obligations.

Before you work with a new client, do you run a credit check on them? We found that 78% of SMEs don’t credit check before bringing on a new client! We understand, especially as a smallbusiness, that time is precious, but the importance of checking new customers shouldn’t be overlooked.

as a consumer credit reporting company, but it also collects information on millions of businesses and provides businesscredit reporting services. Tillful x Experian Partnership The Experian businesscredit score is now in the app and Tillful dashboard! What is a good Experian businesscredit score ?

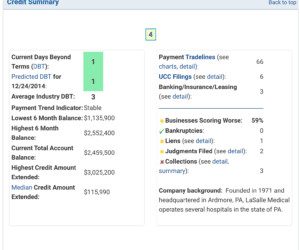

In addition to the businesscredit score , you can also get: Financial stability risk ratings Banking, trade, and collection history Liens, judgments, and bankruptciesCredit limit recommendations. Equifax BusinessCreditRisk Score. A score of 556 is generally considered good credit.

The news is full of doom and gloom about the bank crisis and a potential recession, causing many consumers and business owners to fear the future. A bank crisis does, in fact, have impacts on the economy and can particularly affect entrepreneurs and smallbusiness owners. Banks, by nature, face numerous risks.

As a smallbusiness factoring company, we encourage potential clients to send us their invoices and share how they tackle the invoicing process. Because a fresh set of eyes can shine a light on the gaps in your business. Where are the gaps in your smallbusiness performance? Are you removed enough to see them?

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content