This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Making the decision to file for bankruptcy is far from easy. The trade-off for having your debt eliminated is a long-lasting derogatory mark on your creditreport identifying you as a huge credit risk. Your creditreport sees the effects of a bankruptcy filing for ten years for a chapter 7 bankruptcy.

Filing for bankruptcy sets your credit score back significantly, but you can usually begin to recover within a few months and make meaningful progress within a year. Within two years, your credit score could be even better than before you filed. Filing for bankruptcy is a serious setback, but it’s not insurmountable.

Seventh Circuit Rejects Consumer’s FCRA and FDCPA Claims Arising from Post-Bankruptcy Collection and Reporting Freeman v. The consumer filed for bankruptcy and eventually cured her pre-petition mortgage default through her bankruptcy plan payments. Ocwen Loan Servicing, LLC , No. 23-2512, 2024 U.S. LEXIS 17093 (7th Cir.

But making heads or tails of your business creditreport can be tricky. What is a Business CreditReport? There are three main business creditreportingagencies: Dun & Bradstreet (D&B), Experian , and Equifax. This is really no different than the concept of a personal creditreport.

Your business credit score affects your ability to get loans, enter into leases, and make purchases—and since other businesses, banks, and lenders can check it at any time without your permission, you want to make sure that it’s completely accurate. But making heads or tails of your business creditreport can be tricky.

There are dozens of places where you can obtain your creditreport. The three big credit bureaus, however, are Equifax®, Experian®, and TransUnion®. Often referred to as creditreportingagencies, these companies work independently. CreditReports vs. Credit Scores. Public Records.

A good credit score positions you as a trusted potential borrower with commendable credit maintenance habits. The three major creditreportingagencies in the U.S., Derogatory remarks on your report (though accurate) could also portray you as a bad borrower.

They each have their own formula for reporting your credit score—and none of them actually tell us what that formula is. Here’s what they pay attention to: Payment history (including bankruptcies and judgments). Age of your open credit accounts. Diversity of credit accounts. Check Your CreditReport For Errors.

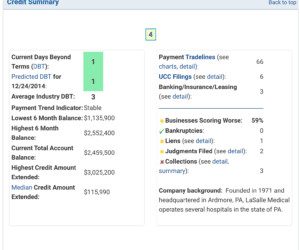

Outstanding debts, liens, bankruptcies, UCC flings or judgments connected to the business. While each creditreportingagency has its own formula for calculating scores, the above are some of the major factors considered when putting together your business creditreport.

The first option involves directly contacting the lender regarding the potential error on your payment history, such as a credit card company or student loan issuer. The next option involves filing a dispute with the creditreportingagency regarding the possible erroneous entry.

Public records usually appear on your creditreport as the result of a financial disaster. Evictions, foreclosures, bankruptcies, and judgments are terrible news for your credit. Each one of these affects your creditreports and scores differently. What Do Public Records Mean on a CreditReport?

Your account might be sent to a collections agency and you might start getting a lot of collection calls. In addition, your lender will report each missed payment to the business creditreportingagencies and/or to personal creditreportingagencies, which can hurt your credit score.

You’ll see them disappear from your creditreport after just two years, though they’ll stop affecting your credit score after one. For comparison, most negative items remain on your creditreport for seven years, and some types of bankruptcy can stick around for as long as ten.

The Major Business CreditReportingAgencies The job of a business creditreportingagency (also called a business credit bureau) is to gather information about your company. A credit bureau gathers details from your previous creditors and other sources and puts that data into a business credit file.

Outstanding debts, liens, bankruptcies, UCC flings or judgments connected to the business. While each creditreportingagency has its own formula for calculating scores, the above are some of the major factors considered when putting together your business creditreport.

The three major credit bureaus, Equifax, Experian, and TransUnion, all offer consumers a free copy of their report annually. Perhaps collection accounts associated with an eviction were subsequently reported inaccurately? In this instance, you can initiate the dispute process with the creditreportingagency.

In the business credit world, there are five main creditreportingagencies. These credit bureaus gather information about your company and resell it to others that want to predict the risk of loaning money to your company. It’s wise to understand who the business credit bureaus are and how they operate.

The Fair CreditReporting Act (FCRA) requires that original lenders or debt collectors that report unpaid accounts to creditreportingagencies include the original date of delinquency that represents the “starting point” for the seven-year period when the account is removed.

Life’s uncertainties—job loss, emergencies, foreclosures, bankruptcies—can severely damage credit. With a commitment to bouncing back, discipline, careful planning, concrete goals, and strategic choices, it is possible to recover from financial troubles and rebuild your credit status.

Checking the business credit scores of the companies you hope to do significant business with helps keep you safely back from the edge. The Fair CreditReporting Act (FCRA), passed in 1970, protects personal credit scores as private. A one-time report from Dun & Bradstreet will cost $121.99.

According to Dun & Bradstreet , they can include liens, judgments, bankruptcies, UCC filings, and business registrations. Derogatory public records are those that contain negative information such as bankruptcies and liens. How long do collections and other derogatory marks stay on your business creditreports ?

Each creditor has a different reporting schedule though, so it may take up to 90 days for the new information to post to your creditreport. It’s important to note that not all lenders send information to all three credit bureaus. Some lenders might send data to only one or two creditreportingagencies.

Outstanding debts, liens, bankruptcies, UCC flings or judgments connected to the business. While each creditreportingagency has its own formula for calculating scores, the above are some of the major factors considered when putting together your business creditreport.

They each have their own formula for reporting your credit score—and none of them actually tell us what that formula is. Here’s what they pay attention to: Payment history (including bankruptcies and judgments). Age of your open credit accounts. Diversity of credit accounts. Check Your CreditReport For Errors.

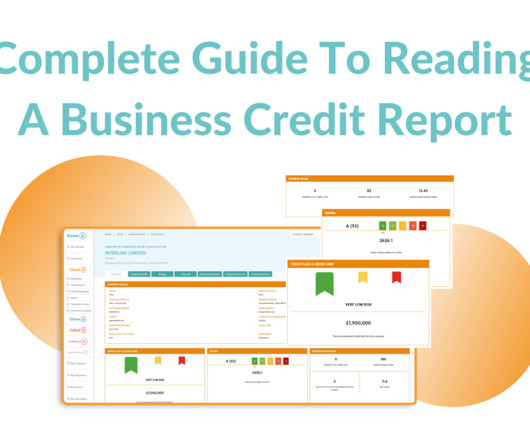

Business creditreport which is also known as a company creditreport, contains information regarding the business, such as ownership information, subsidiaries, company finances, risk scores, and any liens or bankruptcies. In case you purchase any company creditreport it should contain the following information.

Inaccurate Information on Your CreditReport Consumers should regularly check their current credit bureau reports to assess their overall credit rating and look for any potential errors. Each creditreportingagency will provide you a free copy of your creditreport that allows for reviewing your credit history.

Doing business with a company heading into bankruptcy or extending credit to an organization that has a deteriorating financial position are significant risks. A business creditreport can identify adverse situations or warning signs to help you decide if you want to accept the risk.

When you pull a creditreport about your business, you can see exactly how the business creditreporting bureaus rate your creditworthiness and the information others will see when they look. Applying for Credit. There are different types of business creditreports and services available for your business needs.

Experian ’s business creditreports also feature a financial stability risk rating which aims to predict the likelihood of a bankruptcy or payment default in the next year. The scores range from one to five but, unlike the business credit score , a lower score indicates lower risk. Don’t apply for too much credit.

Get your free creditreports at www.annualcreditreport.com or by calling 1-800-322-8228. Review the reports carefully and look for inaccuracies. Notify the relevant creditreportingagency within 30 days of receiving your report. If you see an error, you have the right to have it corrected.

You can get business creditreports from each of the three major business creditreportingagencies, including Equifax, Experian, and Dun & Bradstreet. While Experian and Equifax provide public record searches with their Score Summary reports., How to Check Business CreditReport Instantly.

Your business creditreport is an assessment of your financial health and predicts whether you are likely to pay your bills. Assets, such as property or equipment, that could be sold off in case of financial trouble or bankruptcy will likely raise your business credit score. Debts & Credit History.

Most negative information such as late credit card payments, collection agency activity, and other missed payments toward debts remain on your creditreport for seven years. Bankruptcy is an exception that may remain on your credit bureau report for up to 10 years.

Credit repair services work on behalf of consumers with negative items on their credit history, such as missed or late payments on debts. A credit repair service will access your creditreportingagency files compiled by the three major credit bureaus: Equifax, Experian, and TransUnion.

There is one exception—bankruptcy may remain on your credit bureau report for up to ten years. More precisely, a Chapter 7 bankruptcy will remain for up to ten years, while a Chapter 13 bankruptcy generally remains for seven years. Payments only get reported to the credit bureaus if they are 30 days late.

According to Experian’s The State of Alternative Credit Data whitepaper, traditional credit data includes everything found on business and consumer creditreports as well as the information that’s commonly requested on lending applications, including: Tradeline information Credit inquiries Public records (e.g.

The key metric displayed on a business creditreport is a business credit score. Each creditreportingagency will use slightly different scoring criteria and algorithms, but this score will let you know at a glance the credit-worthiness of a company. Bankruptcies: nine years and nine months.

If you want to know how to rebuild credit, you can start by making timely payments on all available credit accounts and using other strategies explored in this article. 7 Strategies To Rebuild Credit The first step to rebuilding credit involves obtaining a recent copy of your creditreport.

The first negative information that appears on your creditreport is entries regarding late payments or missed payments that are reported to the creditreportingagency. A foreclosure will remain visible on your credit history for seven years from the first mortgage-related account delinquency.

Here is an explanation of the different options that are available through Command Credit, the lowest-priced provider of business creditreports from all of the major business creditreportingagencies. Buy Business CreditReports: The Self-Serve Option.

We get that, for many small business owners, raising your credit score can feel like just another thing on top of a huge stack of to-do’s. Plus, knowing that there are three main business creditreportingagencies ( Experian , Equifax , and Dun & Bradstreet ) can feel a bit overwhelming.

One way for new businesses to build their credit history and obtain a business credit score from creditreportingagencies is by opening net 30 vendor accounts that have lenient approval criteria and offer credit purchases with a 30-day payment window. Burstbiz 2. The Red Spectrum 3.

Unlike a consumer credit score, which uses a fairly standard ranking system, business creditreporting bureaus use different data sets. So, what is a good business credit score ? It depends on which credit bureau you use. What Is a Good Business Credit Score? Equifax Business Credit Risk Score.

If everything goes according to plan, that lets you open new credit accounts despite any missed payments, account defaults, or bankruptcies in your credit history. You’d have a second chance to build a credit profile from scratch. CPNs are definitely illegal, no matter what your credit repair company says.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content