This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

(Photo by Markus Spiske on Unsplash ) When there are time constraints that forestall additional research, denying credit or requiring collateral or some other security is the best way to avoid a decision that results in delinquency and a potential baddebt loss.

We don’t, however, want to minimize the importance of the credit side of the equation. As discussed in a recent post , gathering customer information doesn’t stop with the creditapplication. You put your firm at risk by limiting credit assessments to only new customers, which is too often the case.

Transforming your creditapplication process through digitization not only enhances credit extension capabilities but also significantly elevates the overall customer experience. Evaluating Your Current Processes: To begin, take a critical look at your existing creditapplication processes.

Learn More About YVCM Consulting Case Study: Portfolio Monitoring Pays Off Big-Time About 25 years ago, a credit manager I know saved his company from a seven-figure baddebt loss by monitoring the Internet on his biggest customers. request for substantially more credit, change in leadership, merger or acquisitions, etc.).

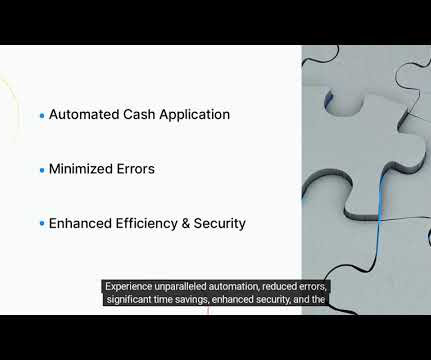

While automating things like remittance processing, creditapplication processing, and portfolio monitoring and analysis will help you improve DSO, there are two types of automation solutions that are proven to significantly improve cash flow. This leads to quicker payments and improved cash flow.

Bust-Out Schemes : Criminals establish fake businesses, submit fraudulent creditapplications, make small payments to build trust, then divert large orders and dissappear, turning receivables into baddebts. Preventing email comprpomise requires verification of changes (payment details, shipping address, etc.)

Contact your customer success manager or email us at info@gaviti.com Join our webinar on Sep 13th to learn more about the new Cash Application module >> CreditApplication Management: Empowering Risk Management and Visibility Avoid high risk customers from the start and monitor ongoing risk as they build a relationship with you.

You can do this quite effectively by having a detailed creditapplication, I’m so much of a proponent of this that I wrote a whole blog dedicated to creating one. A detailed creditapplication does two things, it informs your customer of the terms and conditions of the credit you extend.

This prediction, although bold, is corroborated by the broader economic data, including escalating corporate bankruptcies, tightening loan standards by banks, and the surge in delinquent debt balances and consumer debt. You may also want to tighten your credit hold parameters at this time. Obtain Quotes on Credit Insurance.

Processing Delays There are several AR activities that often take longer than they should and therefore cause delays: processing creditapplications, approving orders, generating invoices, and posting payments. When unobserved risks build up in your AR, the impact will be slower payments and defaults leading to baddebts.

The company ended up writing off millions of dollars in baddebt. In addition, baddebt and concession expenses decreased by several million dollars annually. So far so good, but this company had an Achilles heal. This software firm did not actively manage its AR. Cash flow from AR was well below reported revenue.

How much baddebt does the company have, and how has this changed over time? Are we offering the right amount of credit to customers based on their creditworthiness? Consider these additional KPIs: Baddebt ratio: This measures the monetary value of receivables you believe you cannot collect.

Having credit risk processes in place from the outset is ideal, but credit risk management procedures can be implemented at any stage to reduce your exposure to risk of baddebt write off, improve cash flow and protect your profit Below are a few methods to use for managing credit risk.

Photo by Muhammad Daudy on Unsplash ) The problem with startup companies: there is a high probability they will fail , leaving you with a baddebt on your books. That’s why it is standard to ask on a creditapplications the year in which the business was formed.

Ensure you have alerts set up so that you are aware when a customer is near their credit limit or to know if a customers credit score has changed. Consistency in credit processes reduces baddebt and fosters healthier customer relationships.

During 1995, DSO was reduced by an additional 10 percent, and bad-debt write-offs cut in half. Here are the six other types of AR automation being implemented across the order-to-cash (O2C) spectrum: Online CreditApplications: The best solutions provide approval workflow and automated reference checking.

Who to contact should be information requested on your creditapplication. While it is appropriate to escalate your collection efforts up the chain of command of your primary customer contact, you should not be talking about a debt with other customer employees such as a receptionist, operator or logistics person.

Using the real-time data, you can more easily adjust credit limits effectively to proactively reduce risk of late payments, baddebt, and write-offs. An A/R automation solution can not only help you in the initial creditapplication process, but also to regularly assess a customer’s credit risk on a regular basis.

This is because the higher your profit margins the fewer sales it will take to compensate for any baddebt losses. As your production pipeline approaches full capacity, the fussier you can be about who you grant open credit terms. The question you need to answer is: should credit policy be liberal or conservative?

As a small business owner or executive, managing accounts receivable (AR) and navigating through various credit decisions is an integral part of the job. After all, credit and collections is essential to the performance of your order-to-cash (O2C) process and cash conversion cycle.

Financial Stability : Reducing outstanding receivables minimizes baddebts and improves financial health. Detailed Steps in the Accounts Receivable Process Cycle Step 1: Establishing Credit Policies Define the eligibility criteria, credit limits , and payment terms based on customer risk assessment.

In contrast, profit driven enterprises often miss opportunities because they are too restrictive out of a fear of baddebt losses. A segmentation analysis will help you refine your credit policy guidelines and thereby improve the efficacy of your credit decisions.

Photo by Willian Cittadin on Unsplash ) Neglecting collections can also lead to longer payment cycles, strained client relationships, and an increase in baddebt. This delay in cash inflows can create a vicious cycle, where a lack of working capital stalls the business’s ability to function efficiently.

The worst case scenario is a baddebt loss. For more on credit agreements and the new customer creditapplication process, check out this post. With this in mind, here are seven ways to improve your later phase collection results: Not a subscriber. why don’t you take advantage of a free YVCM subscription?

. • Use Late Payment Legislation as a negotiating tool to get paid more quickly Credit control should no longer be the ‘anti sales’ department by the rest of the company, they should work with all areas of the company to provide good customer service whilst improving cash flow and reducing baddebt exposure.

Credit monitoring and management. Automate the creditapplication process by allowing creditapplication submissions online to both existing and potential customers. This can be especially helpful in maximizing cash inflows and minimizing baddebt. Customized collections strategies.

It also helps provide documentation in the event that your company has baddebt that it is able to take as a tax deduction. Credit management and monitoring. Send online creditapplications to both existing customers and potential prospects. Get alerts in real-time about customers with increased credit risk.

Its creditapplication management module automates the entire credit management process, mitigating the risk of baddebt while also reducing the need for administration costs.

This enables effective credit risk management by limiting loan options to individuals with a specified income level. What is Credit Risk Management Best Practices? Having comprehensive and accurate customer information enhances the effectiveness of credit risk analysis. When designing your credit risk analysis.

Delinquent accounts increase the amount of baddebt your company accumulates and its perceived risk for investors. Manage customer credit risk Maintain a clear credit history for each customer so that you can make informed credit decisions and minimize risk. Company valuation. Reduced liquidity.

Granting credit is an important tool for attracting and retaining customers. However, it is crucial for businesses to perform a credit check on the customers before extending credit, to avoid loss of revenue by way of baddebts. Digital signature in place of a manual signature on a paper application.

Unlike credit or corporate cards, the line of credit offered is for exclusive use at Staples so helps build loyalty and encourage repeat business. And because the trade credit is underwritten by TreviPay, Staples never needs to chase late payments or baddebts.

You can also call a businesses’ references and creditors directly or view their financial statements as part of the creditapplication. If baddebts are increasing, finding their source may uncover problems in your credit approval process.

Cash Flow – A B2B credit card program enhances cash flow through a reduction in the cycle time it takes to close a transaction, whether it be at the point of purchase or a defined payment date, by eliminating float time through the United States Postal Service.

Unlike credit or corporate cards, the line of credit offered is for exclusive use at this retailer so helps build loyalty and encourage repeat business. And because the trade credit is underwritten by TreviPay, the retailer never needs to chase late payments or baddebts.

Unlike credit or corporate cards, the line of credit offered is for exclusive use at this retailer so helps build loyalty and encourage repeat business. And because the trade credit is underwritten by TreviPay, the retailer never needs to chase late payments or baddebts.

Your creditapplication should include all this information. A recent credit bureau report is also helpful in this regard. Your Virtual Credit Manager now offers reasonably priced business credit reports through Accredit, a leading reseller of credit bureau reports.

The accumulation of baddebt is a massive hindrance for businesses that rely on consistent cash flow in their accounts receivable. Piling baddebt reduces your companys expected revenue and limits your ability to reinvest liquidity into business operations. The BadDebt Spiral.

Without proper credit assessments and checks, businesses expose themselves to significant financial risks, including cash flow disruptions and potential baddebts. Manual Application Processing: Accommodate traditional creditapplications by allowing for manual data entry and assessment, ensuring no customer is left behind.

About 25 years ago, a credit manager I know saved his company from a seven-figure baddebt loss by monitoring the Internet on his biggest customers. Ongoing Portfolio Monitoring was critical to turning up the customer intelligence that avoided a huge baddebt loss. A Case in Point.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content