This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In our case, we found a continued interest in collection technique and strategy, as well as in fighting credit fraud. What follows is a summary of the three most read article for the 12 months ending in October 2024, and links to the originals. To avoid this, collections should begin within 3-7 days of the due date.

Here’s a warning to trade creditor’s from a major commercial credit bureau (from CreditSafe’s Cost of Late Payments report). If you are extending credit to other businesses, it’s high time you began watching your customers closely for late payments and other signs of distress.

The Customer Delinquency Challenge Successful accounts receivable (AR) management involves minimizing past due balances to ensure steady cash in-flows and limit baddebt losses. When you do eventually get paid, you recover the cost you expended in fulfilling the customer order less the cost of collections and any interest on loans.

This mindset often leads to underinvestment in collections efforts, and when budget cuts are necessary, accounting departments like collections are typically the first affected. However, maintaining a steady cash flow is essential for business survival, and efficient collections directly impact the bottom line.

The better you know a customers, the easier it is to make a correct credit decision. One of the biggest challenges for any credit function is making a valid decision when information is lacking. That’s why standard procedure calls for gathering additional credit information until a comfortable decision can be made.

Commercial collections is no different. Collection myths can be found at the very root of bad decisions as well as informing counter-productive activities. Adhering to collection myths more often than not leads to bad outcomes. Simply put, collection myths get in the way of doing the best job possible.

Contacting customers to pay past due amounts (collecting) is an essential element of accounts receivable (AR) management. For most firms, late customer payments are a frequent occurrence and collecting them can be a difficult task. Collections also has to be done effectively with minimal alienation of customers.

Credit Policy is an inextricable part of a company’s Sales Policy. If you choose to sell on open credit, the terms you offer are in effect part of the price. If you discuss credit terms with a competitor, you are in violation of anti-trust statutes forbidding price fixing. What’s Right for Your Firm?

Effective collections are crucial to maintaining a healthy cash flow and the financial stability of your company. If your business is struggling with cash flow or AR balances are growing, it could be a sign that your collections policy requires updating. There are a myriad of issues that can affect collections.

If you sell on open credit terms, you need to plan on having to expend time and resources collecting from those customers that don’t pay when due. No matter how much effort you put into evaluating customer credit, some customers will not live up to your expectations. You need to be doing the right things.

As a consequence, commercial accounts receivable (AR) portfolios are at an increasing risk of suffering baddebt losses. The immediate precursor to baddebts is increasing percentages of delinquent receivables, especially in the over 60 and 90 day aging categories. Commensurate with that, the Federal Reserve Bank of St.

As a business owner, it’s essential to understand and manage credit risk to maintain a healthy cash flow and avoid financial losses. Credit risk is the potential for a borrower to fail to repay a loan or credit extended to them. When you sign up for a free Know-it account you’ll also get a free business credit report!

Approving a customer for credit terms is merely the first step in an open credit relationship. Economic circumstances may cause you to tighten your credit policies and customer credit limits. In this case, ongoing Portfolio Monitoring was critical to turning up the customer intelligence that avoided a huge baddebt loss.

Starting in October, free subscribers will only receive the introductory section of our weekly articles. Plus, you get full access to our growing archive of over 100 articles! Assuming the supplier has a line of credit, the longer a customer delays payment the more interest the supplier has to pay the financial institution.

Photo by DESIGNECOLOGIST on Unsplash Editor’s Note: To start off the New Year, we’re bringing back three of the most popular YVCM articles from 2023. We’ve condensed the articles to save you time, but have also provided links to the originals should you want to take a deeper dive. Update your customer master file.

Processing Delays There are several AR activities that often take longer than they should and therefore cause delays: processing credit applications, approving orders, generating invoices, and posting payments. Credit evaluations, however, often take time. Plus, you get full access to our growing archive of over 100 articles!

If your sales are consummated via payment at the point of sale, which may involve “pay with order” or “pay on delivery” protocols involving a credit card or an online e-payment product, managing Accounts Receivable (AR) will not be big issue for you. The company ended up writing off millions of dollars in baddebt.

The following excerpt is from a recent Forbes article : “ According to interviews AccessOne conducted with 47 healthcare billing executives, 43% of providers reported increases in patient requests for payment plans even as hospitals face their own financial struggles, and 40% report an increase in baddebt.

Open Credit Terms dominate the Business-to-Business (B2B) marketplace. Photo by Jamie Street on Unsplash There are two types of credit risk that arise from selling on open credit terms: Customers paying beyond terms (past due) reduce your cash flow. These baddebt losses can put your own business at risk of failure.

Two weeks ago we recapped the three most read articles from 2023: identifying red flags, understanding why customers pay late, and the secrets of successful collectors. Then last week we looked at credit hold best practices. From a credit management perspective, these are largely reactive topics.

In this article, we explore the advantages of autonomous finance, especially as it relates to accounts receivable, and at what point your company should consider employing them, so you can decide if it’s a worthwhile investment for your business. What are the Benefits of Autonomous Finance in A/R Collections?

Supply chains threatened by soaring insolvencies Recent data has revealed the average baddebt for UK SMEs is £16,641, a spike of 61% in a year! Baddebts If the insolvent company owes you money, you may not be able to recover the debt, or you may only receive a fraction of what you are owed.

Starting in October, free subscribers will only receive the introductory section of our weekly articles. Plus, you will get full access to our growing archive of over 100 articles! Now that you understand that your customer has become a liability, it’s time to review their credit worthiness again so you can make informed choices.

Maintaining a healthy cashflow through credit control is crucial for the long-term success and sustainability of any enterprise, especially against the backdrop of soaring insolvencies and record instances of late payment. One effective strategy for achieving this goal is to implement a robust credit control system.

In this article, we’ll outline 15 actionable steps that can help you significantly reduce debtor days and optimise your cashflow! Evaluate and improve your credit terms Begin by assessing your current credit terms and ensure they are reasonable and aligned with industry standards. Struggling for time?

As a business owner, it’s essential to understand and manage credit risk to maintain a healthy cash flow and avoid financial losses. Credit risk is the potential for a borrower to fail to repay a loan or credit extended to them. When you sign up for a free Know-it account you’ll also get a free business credit report!

As a business owner, it’s essential to understand and manage credit risk to maintain a healthy cash flow and avoid financial losses. Credit risk is the potential for a borrower to fail to repay a loan or credit extended to them. When you sign up for a free Know-it account you’ll also get a free business credit report!

Poor Vetting Process for New Customers When you extend credit, you must do so because you can reasonably expect to get paid that money eventually. Failure to properly vet customers opens the door to delayed payments, baddebts, court battles, and worse. Standard options include money orders, checks, ACH, credit cards, and cash.

Many businesses that owe money to creditors use debt collectors, who work for a fee or a portion of the total amount collected. Some debt collectors are also debt purchasers; these businesses buy debt below its face value and then make an effort to collect the entire amount owed. Key Takeaways.

This article explores the benefits of B2B accounts receivable automation and its key features and demonstrates why it’s time to say goodbye to manual work. Faster Payment Cycles Automated accounts receivable systems streamline the invoicing and payment collection processes, resulting in faster payment cycles.

As a business owner, it’s essential to understand and manage credit risk to maintain a healthy cash flow and avoid financial losses. Credit risk is the potential for a borrower to fail to repay a loan or credit extended to them. When you sign up for a free Know-it account you’ll also get a free business credit report!

Extending trade credit to small and medium-sized businesses (SMBs) can be a smart decision for enterprise organizations that want to increase growth. However, managing a high volume of frequent payments manually hasn’t been easy – until trade credit automation platforms emerged in the market. Benefits of Trade Credit Automation.

Effective credit control is crucial for maintaining a healthy cashflow and financial stability. By implementing a well-structured credit control process, businesses can mitigate the risks associated with late payments and baddebts, ensuring a steady stream of revenue.

Rather than providing articles like a typical blog, his site includes accounting tutorials and extensive Q&A about each topic, along with practice quizzes and puzzles to reinforce your knowledge. Who it’s for : Anyone struggling to learn accounting concepts such as debits and credits or accrual vs cash basis accounting.

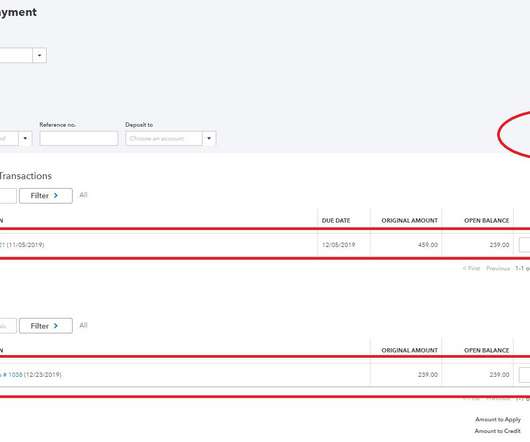

In this article, we’ll look at the best ways to write off an invoice in QuickBooks. There are a couple of reasons why you might want to write off an invoice in QuickBooks : Baddebt. This could result in you remitting sales taxes you never actually collected. How to Write off a BadDebt Invoice in QuickBooks.

Offering trade credit can bring a huge boost to your business! One effective strategy that accomplishes both goals is offering trade credit. This is an arrangement where businesses extend credit to their customers, allowing them to purchase goods or services and pay at a later date.

In today’s fast-paced and interconnected world, credit control has become a vital aspect of financial management for businesses. Traditionally, credit management involved manual processes and relied heavily on human intervention, which often proved time-consuming and prone to errors. Check out this short demo to see how-it works!

As a business owner, it’s essential to understand and manage credit risk to maintain a healthy cash flow and avoid financial losses. Credit risk is the potential for a borrower to fail to repay a loan or credit extended to them. When you sign up for a free Know-it account you’ll also get a free business credit report!

A recent article suggested that the ‘gig economy’, consisting of apps such as Uber and Airbnb employs no fewer than 1 in 10 working adults in the UK. Whilst there can be found some criticisms, the above article notes that the amount of people earning an income from these apps has doubled in recent years. That is approximately 4.7

So a career in various credit management roles before JSP Credit Management being born of over 15 years has left us extremely well placed to pass comment on some potential causal factors affecting non-payment. However, we are not just here to slap commission rates on provisioned debts for companies and set about recovering it for them.

For B2B businesses, financial management involves several specific considerations, including managing cash flow, understanding credit terms, and leveraging financial tools to optimize business performance. Understanding and managing these credit terms is vital for maintaining healthy cash flow and minimizing financial risk.

In this article, we’ll take a close look at adjusting entries for accounting purposes, how they are made, what they impact, and how to minimize their impact on your financial statements. . Every transaction in your bookkeeping consists of a debit and a credit. Does this mean your books aren’t as accurate as you thought?

The bad news is that nearly 21 percent of last year’s startups will fail this year leaving you with a baddebt on your books if you sold to them on credit terms. This is why age is an extremely important consideration when extending credit. The good news is that this is an increase in potential customers.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content