This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Monitoring and evaluating the creditrisk posed by public companies and other large firms differs significantly in comparison to small and mid-sized businesses. For a masterclass on Strategic Collections , join David Schmidt online November 19, 2024, at 1:30 PM EDT. Register Do you need help improving cash flow?

This blog breaks down the pros, cons, and what financial institutions should consider when evaluating their risk rating approach. Is a 2D risk rating model still worth it? An effective risk rating framework is probably the single most important tool a bank can use when it comes to managing creditrisk.

As rates stay high, concerns about creditrisk and borrower health are top of mind for bank and credit union leaders, especially as it relates to lending to small businesses. Early 2024 figures show a dip in DSCR to 4.62x. However, recent data from Abrigo shows that privately held companies across the U.S.

Issuance of commercial mortgage-backed securities (CMBS) rebounded sharply in 2024, with volume jumping 155% year-over-year to more than $100 billion. However, office properties struggled to attract lenders, with their share of CMBS issuance shrinking to under 8% by late 2024, compared to 20% in early 2023.

TreviPay offers a wide range of solutions for the airline industry, including payment and accounts receivable management and creditrisk outsourcing. TreviPay helps take the risk by extending credit and guaranteeing corporate payment while eliminating time-consuming manual billing and invoicing.

Based on comments from the Abrigo Advisory Services team and our bank and credit union clients, executives will have their work cut out to manage profitability, balance sheet growth, and creditrisk. Still-elevated interest rates are running into declining consumer purchasing power, which stands to add pressure to creditrisk.

Conclusion Takeaways from ThinkBIG 2024 Financial institutions can navigate the complexities of the current economic landscape while maintaining strong customer relationships by investing in community engagement, compliance as a value-add, technological integration, and understanding generational shifts. Learn more at abrigo.com/thinkbig.

Fortify your creditrisk management framework How to prepare your organization for scrutiny of its creditrisk management practices during your next exam or review. . You might also like this whitepaper, "Stress Testing: Managing Capital Levels and CreditRisk." keep me informed. Know your limits.

For an Introduction to Business/Commercial Collections, join David Schmidt online November 12, 2024, at 1:30 PM EDT. Webinar Registration Do you need help assessing your customers’ creditrisks? To receive new posts and support my work, please subscribe for just $5 per month ($49 yearly).

When we first think about creditrisk, our minds focus on the financial status of the company in question. To manage the risk that a customer might default, companies implement credit and collection policies and procedures. To receive new posts and support my work, please subscribe for just $5 per month ($49 yearly).

Consistently rated a top industry event by attendees, ThinkBIG brought together 650 people from banks, credit unions, and partners in 2023. The ThinkBIG 2024 conference is June 3-6 in Phoenix, Arizona, and with 99% of last year’s attendees saying they would recommend the conference to others, Abrigo expects another large crowd.

The Altares report reveals a record explosion in insolvencies in 2024, accentuating non-payment and insolvency risks. The challenges for Credit Management and key strategies for securing receivables.

FDIC list The state of acquisitions in a rising rate environment According to the FDIC, there were 44 banks on the problem bank list in the third quarter of 2023, and the agency expects that number to continue to climb in 2024. Watch this webinar, "Understanding audit and regulatory expectations for CECL."

Credit unions only make 2.4%. But both banks and credit unions have substantially increased their lending activity through 7(a) since 2020. Banks have issued 59,833 approved 7(a) loans so far in fiscal 2024, up 53% from 2020. Credit unions have handled 1,634 approved 7(a) loans this year, up nearly 40% from 2020.

Likewise, the construction and business services industries, accounting for nearly 20 percent of insolvencies last year, are projected to remain the hardest hit in 2024. percent in 2024 — that’s roughly one in twelve. It will also help your prioritize your credit reviews as recommended in item #1.

Prepare with this checklist: 4 Areas to check before bank and credit union exams. DOWNLOAD Strategies for 2024 Key components of managing interest rate risk These five areas of focus can help financial institutions improve their standing and prepare for the future. Upcoming exam?

(Photo by Melinda Gimpel on Unsplash ) The American Bankruptcy Institute recently reported that, “The 6,067 total commercial chapter 11 bankruptcies filed during the first nine months of 2024 represented a 36 percent increase over the 4,561 filed during the same period in 2023.” This initial uptick is only expected to get worse.

Developing a strategy for each problem loan should be based on factors such as negotiating positions, collateral status, and the relationship. How is your loan review function performing?

Scottish FinTech Know-it has revealed it will enter the Australian market in 2024, as part of its global expansion strategy. This strategic move aims to deliver Know-it’s credit management solution to the Australian market, ensuring that Australian SMEs have access to the platform to effectively manage their credit control process.

Takeaway 3 With lower interest rates nowhere in sight, lenders need to monitor and adjust lending and underwriting strategies based on their own institution’s creditrisk profile. Almost half sought credit to grow their businesses, and 28% applied to make repairs or replace capital assets. 1 appeared first on Abrigo.

Papers, infographics on risk management Resources related to banking headlines were popular For banking risk and accounting staff, managing challenges tied to interest rates, liquidity, and credit portfolios will remain top-of-mind in 2024. The popularity of this whitepaper on stress testing, then, is understandable.

May We H-it London For Accountex We had a great time talking to new and existing clients whilst showing new audiences how Know-it helps businesses mitigate creditrisk, reduce debtor days and boost cashflow! We are excited to be heading back to Accountex in May 2024 to exhibit at an even bigger stand!

For example, finance teams might apply it towards cash flow forecasting, creditrisk assessment and identifying the best investment opportunities. The post Best 5 Autonomous Finance Tools for 2024 appeared first on Gaviti. Predictive analytics. Schedule a demo to learn more. Speak to a specialist today!

The Fed’s latest Small Business Credit Survey , conducted in 2023 and released in 2024, found that nearly 60% of employer firms had sought financing in the previous 12 months. Almost half sought credit to grow their businesses, and 28% applied to make repairs or replace capital assets.

Pruis Examining federal Call Report data from 2016 to Q1 2024 for banks with assets of $70 billion or less, Cornerstone found that only one in 10 institutions that started in 2016 with less than 18% of its portfolio in C&I was able to increase that percentage by 2023. What will need to change for solid commercial credit analysis ?

How industry analysis can improve your creditrisk management Understanding your customers' businesses leads to better loan pricing, structure, and risk management. You might also like this webinar series, "Tackling common creditrisk questions during challenging times." Get more creditrisk best practices.

According to the OCC, examiners should "determine the suitability of governance processes, including acquisition or retention of qualified staff, when the board or management undertakes significant changes" related to: M&A System conversions Regulatory requirements The implementation of new, modified, or expanded products and services (such as (..)

Preparing your credit administration for the next cycle Financial institutions should consider these tips for maintaining an efficient credit process throughout the year. You might also like these on-demand webinars tackling common creditrisk questions. Discover options for loan policy review assistance.

In AGC’s 2024 outlook report , 64% of contractors named rising interest rates and financing costs as one of their biggest concerns. Given the importance of cash flow management in construction, these pressures may point to underlying construction lending risks that may outweigh returns. Stay up to date with CRE advice.

Credit spreads can be two to three hours faster per loan when creditrisk software auto-imports financial data from the individual’s bank accounts and automatically creates a personal financial statement. The analyst can focus on analyzing large, complex scenarios rather than data entry and spreadsheets.

1, 2024, and report for the first time by June 1, 2025. 1, 2024, is the earliest compliance deadline. Despite the seemingly long runway to prepare, it's not too early to get a handle on the new requirements and how they will affect a bank or credit union. Talk to a specialist to learn more.

The risk of failure diminishes as businesses mature and grow, but the problem for any business selling other firms on open terms is the high number of organizations that are relatively young. That’s why it is standard to ask on a credit applications the year in which the business was formed.

Perhaps they might aim to reduce inventory to 80 days by the end of the first quarter of 2024. For example—perhaps you have a manufacturing customer with a 90-day inventory turnover, while the industry average is 60 days. This excess inventory could be costing them significant amounts of money. Read the buyer's guide to lending solutions.

The process culminates in a forum that combines our credit analysts and top-down global macro strategists to discuss the CANDIs' output through the lens of the credit cycle. These indices measure our analysts' assessment of the credit outlook and odds of a crisis in the industries they cover, respectively.

These account provide a serious creditrisk, and should not be approved for open credit terms. When an otherwise good customer because a habitual debtor, their credit limit should be revoked. Recovering what you are owed by this type of debtor requires an aggressive, though still professional, collection effort.

That timeline would put the compliance deadline around October 2024. Whitepaper Lending & CreditRisk Loan Origination System How Many of These Origination Frustrations Can Your Financial Institution Avoid? Compliance would be required 18 months after the final rule is published. The final rule is expected by March 31, 2023.

except if they enable you to secure an additional customer whose business is contributes significant profits, and whose creditrisk is low. The good news is that until Wednesday May 1, 2024, annual subscriptions are only $29.40. Your credit agreement should include the assessment of late charges on past due balances.

The Fed’s latest Small Business Credit Survey , conducted in 2023 and released in 2024, found that nearly 60% of employer firms had sought financing in the previous 12 months. Almost half sought credit to grow their businesses, and 28% applied to make repairs or replace capital assets.

Takeaway 3 Utilize guidance lines to streamline the approval process for customers with fluctuating credit needs Fine-tune annual review Keeping annual review simple Annual loan reviews are a critical component in monitoring the health of a credit after it is initiated. How Strengthen your risk rating system.

Chapter 11 filings, used by businesses hoping to reorganize, have increased by 34 percent in the first six months of 2024 compared to last year. To continue reading and learn six financial markers that suggest a customer’s business is headed in the wrong direction, you must be a paid subscriber to Your Virtual Credit Manager.

Show your board of directors and leadership an outline of what it will take to prepare for FedNow at your institution. Show your board of directors and leadership an outline of what it will take to prepare for FedNow at your institution.

Modern check fraud detection software enhances check verification processes with several sophisticated tools Introduction Why counterfeit check detection matters in 2024 Financial fraud is becoming more sophisticated in today's world, and counterfeit checks and duplicate check deposits are significant threats.

Reading Time: 4 minutes As the Head of CreditRisk at Biz2credit and Biz2X, I manage a team of risk and data science processionals across North America and India, focusing on credit and price decisioning, automation and efficiency in customer journey, and portfolio risk management.

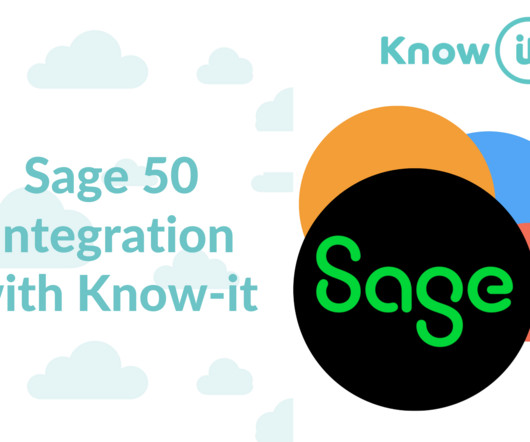

We are excited to announce our first platform update of 2024! Your business can sign up to Know-it in seconds and implement a robust credit management process that will save time through automation. Know-it now integrates with Sage 50.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content