This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When we first think about creditrisk, our minds focus on the financial status of the company in question. To manage the risk that a customer might default, companies implement credit and collection policies and procedures. As you can see, fraud can occur at any point in the customer lifecycle.

Personalized Touch with Efficient Service Can Boost Lending Banks and credit unions can boost business lending by combining a relationship focus with transaction-oriented processing. . Takeaway 1 Many banks and credit unions want to win more business loans but will face higher rates and more competitors. Streamlined, Quick.

Managing creditrisk for B2B customers is critical for seamless order to cash (OTC) and working capital cycles. Businesses that follow traditional reactive strategies in OTC processes may find it difficult to collect at-risk future invoices, likely leading to large invoices going delinquent.

Managing creditrisk for B2B customers is critical for seamless order to cash (OTC) and working capital cycles. Businesses that follow traditional reactive strategies in OTC processes may find it difficult to collect at-risk future invoices, likely leading to large invoices going delinquent.

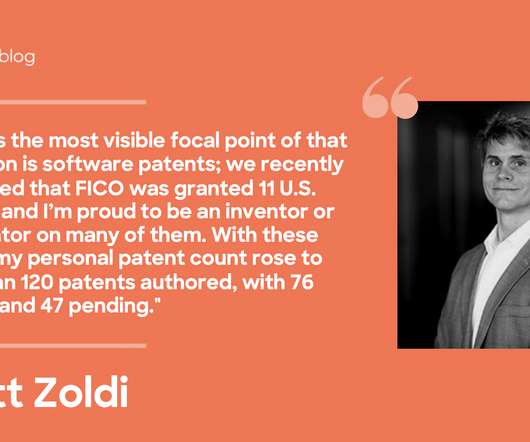

Reflections 2022: The Power of Patents and the People Behind Them. In 2022, FICO was granted 11 new U.S. Mon, 12/12/2022 - 16:00. As 2022 draws to a close I am reflecting on what has been a very challenging year for the world at large. software patents. FICO Admin. Tue, 07/02/2019 - 02:45. by Scott Zoldi.

Addressing Portfolio Risk in Economic Uncertainty: Part 3 (2022). Building portfolio risk resilience into customer management. Thu, 05/12/2022 - 07:46. Thu, 12/08/2022 - 16:00. Of course, creditrisk management is only one aspect of portfolio health. Saxon Shirley. by Jim Patterson.

It will reduce your Accounts Receivable (AR) balance and the associated elevated creditrisk inherent in a larger AR. Getting customers to pay now rather than later reduces the risk of a default down the road. Invoices need to be generated and transmitted the same day as the transaction or at latest the morning following.

Clear from your AR ledger as many of the clutter transactions as possible. Match as many unapplied payments and unapplied credit memos to open invoices, deductions, and debit memos as possible. Refresh the creditrisk ratings and credit limits of customers that have not been updated within the past two years.

Takeaway 1 Some financial institutions have a budget surplus this time of year, and these funds can be spent now to help growth in 2022. Takeaway 2 Excess budget funds can also be used to help mitigate risk in areas such as the BSA department or loan review. Streamline and systematize loan review for 2022. billion from $515.3

Takeaway 2 Reporting tiers and their deadlines are based on the number of covered transactions to small businesses that a lender originated in 2022 and 2023. Despite the seemingly long runway to prepare, it's not too early to get a handle on the new requirements and how they will affect a bank or credit union.

That has top bank and credit union leaders looking to continue the advances in digitalization that have helped them through the pandemic. Indeed, 35% of CEOs say investing in digitalization is their top business opportunity in 2022, according to the Independent Banker’s annual Community Bank CEO Outlook survey. keep me informed.

You might also like this webinar, "Return to basics: Asking the right creditrisk questions." How broad a field does loan review need to plow to unearth potential creditrisks and assess overall credit quality? Scope in loan reviewing What is the scope of an adequate loan review?

After the success community banks and credit unions had helping businesses in their local communities with lending during the pandemic , financial institutions continue to turn to small business loans as a source of portfolio growth. Lending & CreditRisk. Lending & CreditRisk. Lending & CreditRisk.

Is growing the small business loan portfolio on your bank or credit union’s agenda? A recent survey by Abrigo found that 87 percent of banks surveyed are working to win more small business loans in 2022. Lending & CreditRisk. Lending & CreditRisk. Portfolio Risk & CECL. Learn More.

Top 5 Decision Management Posts of 2022: AI and Digital Jane. Wed, 05/25/2022 - 03:43. The promise of AI and FICO Platform dominated the top posts of 2022 in the Decision Management category. The promise of AI and FICO Platform dominated the top posts of 2022 in the Decision Management category. Saxon Shirley.

You might also like this webinar, "Return to basics: Asking the right creditrisk questions." Introduction A few good men and women In previous articles, we have explored the objectives of a loan review and creditrisk review system in general.

In its 2022 Commercial Real Estate Lending update , the OCC advised that staff members who manage real estate and construction lending risk should report to the credit department of a bank rather than to the real estate department. Read the whitepaper, "Red flags and warning signs of contractor failure."

The unusual circumstances make effective loan pricing more imperative than ever for banks and credit unions. Excess liquidity is persisting into 2022, affecting balance sheets and capital and squeezing net interest margins further as banks and credit unions deploy more assets in the lower-margin investment portfolio or in plain cash.

Banking reports to inform risk management and strategy These reports on capital, growth, and liquidity help financial institutions spot warning signs. Takeaway 3 Banking intelligence that's purpose-built for banks and credit unions combines analytics and intuititve dashboards.

Fraud trends for financial institutions to watch for in 2023 Financial institutions should not expect a slowdown of any of 2022’s fraud trends. You might also like this resource: "BSA/AML Risk Assessment Checklist." Financial institutions should not expect a slowdown of any of 2022’s fraud trends. Lending & CreditRisk.

Not surprisingly, then, digital/online account opening solutions for consumers and digital account opening solutions for commercial or small business firms are among the top types of new systems banks are looking to select or replace in 2022, according to Cornerstone Advisors. Lending & CreditRisk. Learn More. Learn More.

billion in fraudulent transactions, a staggering 47% of which were check fraud. One would think as technology improves so would the safeguarding features around monetary transactions. Cybercriminals, Fraudsters, and the Dark Web – What to Watch for in 2022. Lending & CreditRisk. Portfolio Risk & CECL.

T he CBOT enforcement action states that the bank failed to report hundreds of suspicious transactions to FinCEN even after the bank became aware that specific customer s were involved in criminal investigations. If you know you have questionable activity in your transaction monitoring, slow down and report. Learn More.

The below will guide you through a few easy steps to identify if your credit landscape is due an upgrade. CreditRisk Management Software for Effective Credit Control Proactive creditrisk management is a must to support a healthy business strategy.

Spreadsheets and then ERPs were the beginning of digital adoption in finance, which digitalized the manual recording and processing of finance and accounting transactions. A study by Deloitte foresees how automation and blockchain , among others, can transform finance transactions touch-less and self-serving.

There are a number of elements that make up your credit report, including personal information, your credit account history , and your credit inquiries. Credit bureaus receive this information from your lenders and creditors. FICO® Scores are used to determine whether you are a good creditrisk for future lenders.

These changes have impacted lending from mortgage applications, refinancing and other forms of consumer credit. To add to the reduction in demand, Centrix’s Keith McLaughlin stated in a Newstalk ZB interview , that it was not only higher risk borrowers affected by the changes to the legislation.

Especially, how to price loan products for small businesses so as not to crush demand (which is strong due to recession) but also adequately account for the risk that may be entering the economy due to a weaker economic environment. Upcoming Federal Reserve Policy in 2022. Determining CreditRisk for Business Borrowers.

Know-it helps businesses make sense of their sales ledger, better know their customers and automate the credit control process end-to-end. This helps businesses mitigate creditrisk, reduce debtor days and boost cashflow with ease. Trend five: The rise of PaaS Retaining customers is something every business must focus on.

Know-it helps businesses make sense of their sales ledger, better know their customers and automate the credit control process end-to-end. This helps businesses mitigate creditrisk, reduce debtor days and boost cashflow with ease. Trend five: The rise of PaaS Retaining customers is something every business must focus on.

They’re also sound business practice and a solid pathway for dealing with customers – irrespective of where business is being transacted. Plenty still have siloed data across marketing, creditrisk, customer management, fraud, compliance, and collections operations. Source: fca.org. Structure of Consumer Duty. Peter Lemon.

Know-it helps businesses make sense of their sales ledger, better know their customers and automate the credit control process end-to-end. This helps businesses mitigate creditrisk, reduce debtor days and boost cashflow with ease.” “Fintech’s are known for their disruptive innovations, and 2023 will be no exception.

The subjective nature of real estate pricing makes for easily manipulated transactions that run through financial institutions. Credit: Brian Koppel, Reel to Real Filming Locations blog According to a Global Financial Integrity (GFI) study , an estimated $2.3 billion was laundered between 2015 and 2020 through the U.S.

Banks & credit unions recognize the importance of new deposits After years of consistent deposit growth, financial institutions have faced a shift recently, with deposits declining since 2022. Build stronger relationships by recommending deposit products based on customer transaction behaviors.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content